By Mark Stoeckle

April 24, 2020

After coronavirus (COVID-19) fears began shuttering communities and large parts of the global economy in late February, the stock market sank more than 33% in a matter of a month. As frightening as that sounds, it’s important to remember that in reality, many investors haven’t lost anywhere near as much. In fact, typical investors with 60% of their portfolios in stocks, 30% in bonds, and 10% in cash are likely down only about 10% through the end of March, as bonds have gained ground while stocks have fallen.

In this COVID-19-driven market selloff, it’s been asset allocation, not market timing, that has helped investors stave off steeper losses.

The fact is, many investors don’t put all of their money into stocks. They diversify their holdings, investing some in equities for growth, some in bonds for stability, and some in cash for protection for a rainy day. How investors choose to divide their portfolios among these disparate assets is known as asset allocation.

And in this COVID-19-driven market selloff, it’s been asset allocation, not market timing that has helped investors stave off steeper losses. This has enabled them to stay invested and stick with their long-term plans even under trying circumstances. Going forward, your mix of stocks, bonds, and other assets is also likely to explain the majority of your investment performance over the long run.

How Asset Allocation Helped in the COVID-19 Crash

There are a number of factors that determine how much of your money should be invested in stocks, bonds, and other assets. Those considerations must balance your long-term need for investment growth with your overall risk tolerance (see our Insight “Asset Allocation Provides Discipline to Meet Long-Term Objectives”).

A back-of-the-envelope way to think about it is to assume your money can be split into three buckets. Any funds that you’ll need to tap within a year or two probably belongs in your cash bucket, where there’s no risk of losing any principal. Money that you’ll need within the next five years, perhaps for a down payment on a home or for college bills, should largely be in bonds. And anything that you won’t need to touch for five years or longer belongs in stocks, because equities are the one asset that can outpace inflation over many decades.

This means when you’re in your thirties, 70% or more of your portfolio might belong in stocks. But as you age, a greater percentage of your portfolio will shift to bonds and cash. That’s why someone in their forties might limit their equity exposure to around 60%, while those in their 50s and older might have more than half of their portfolios in bonds and cash.

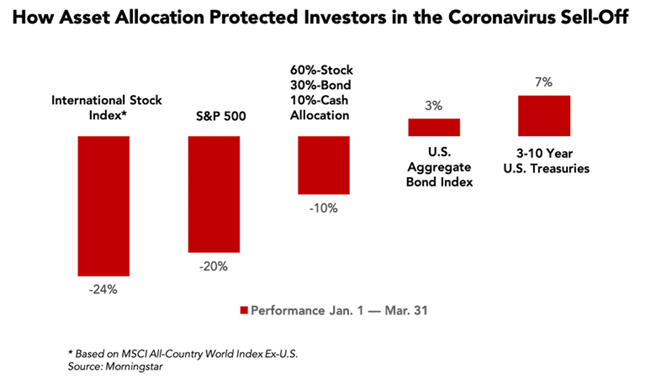

This is critical to understanding how asset allocation affected investors’ performance early on in the COVID-19 downturn. While U.S. stocks fell 20% this year between January 1 and March 31, and international equities lost 24%, U.S. corporate bonds gained 3%. Meanwhile, cash maintained its principal value, while intermediate-term government bonds gained 6.7% during this market selloff, as fearful traders moved out of stocks and into the perceived shelter of Treasury debt. By dividing your holdings among different assets, you can reduce losses when any single investment is melting down. Being appropriately diversified this way should give you sufficient courage to stay invested even in scary times.

How Rebalancing Will Help You Stay Invested the Right Way

After you determine what your proper mix of stocks, bonds, and other assets should be, your job isn’t over. You must also be willing to maintain that asset allocation for your strategy to work. This is another way asset allocation can keep you disciplined.

For example, say you started with $10,000 in the market on Jan. 1, investing $6,000 of that in equities, $3,000 in U.S. government bonds, and $1,000 in cash. After stocks fell 20% by March, your original $6,000 in equities shrank to $4,800. And after government bonds rose more than 6.7%, your $3,000 fixed-income allocation rose to $3,200. In other words, your original 60%-stock/30%-bond/10%-cash strategy effectively shifted to a 53%-stock/36%-bond/11%-cash approach. This may be too conservative for your long-term needs if you leave things alone.

A proper asset allocation strategy requires that on a regular basis, perhaps every six months or annually, you “rebalance” your portfolio so that it reverts to your pre-determined mix. In this example, your asset allocation discipline would require you to buy more shares of your stock funds by selling some of your bonds and using some of your cash to bring back your equity allocation to 60% of your overall portfolio.

It may take some courage to rebalance into a volatile market, but keep in mind that you would be buying additional shares of your stock funds at a much lower price than they were trading at the start of the year. Remember the point of establishing a long-term plan is to keep you on the right path, and rebalancing your asset allocation will allow you to do that in a programmatic way that’s easy to follow.

For more insights, read our article: "How to Invest in Anxious Times"