January 19, 2017

Even as consumer confidence approaches a new 10-year peak, spending habits today bear little resemblance to the last time consumers were this optimistic.

Retail has always been a seasonal business and most consumer companies live and die based on their performance during the holiday shopping season. Last year, as Cyber Monday overtook Black Friday as the preferred holiday shopping date and venue, a number of themes have emerged that reflect the ongoing evolution of today’s consumer. Our interview with Consumer analyst, Dave Schiminger, provides insight about the significant shift in the way people spend money.

Consumers are spending more on "experiences" rather than "things."

What is the state of the consumer today?

Overall, the consumer is feeling more optimistic. With low unemployment and modest increases in wage rates, personal income and spending levels are rising, albeit slowly. Deflation in food prices and, until recently, gas and energy prices are giving consumers more spending capacity. Mortgage interest rates that remain low based on historical levels are also benefiting consumers. However, rising health care and rent expenses remain headwinds. With the S&P 500 at record levels, consumer confidence is approaching 10-year highs. The consumer is spending, but remains somewhat cautious.

How have consumer shopping behaviors changed?

Today, consumers live in an omnichannel world, where they have the ability to shop seamlessly across channels, whether it’s online (using both desktop and mobile devices), in brick-and-mortar stores, or by telephone. Driven by the increasing utilization of mobile devices, e-commerce continues to gain share at the expense of brick-and-mortar stores. Today, shoppers can cross back and forth across these many channels, at different times and for different reasons. These channels determine how consumers conduct research, how they shop, and where they ultimately make purchases. They shop on their smartphones to compare prices on almost any item, at any time and wherever they are. As a result, the demand for value, convenience, and service has become more pronounced.

This has had a tremendous impact on both mall retailers and the department stores. Within the mall channel, Aeropostale and PacSun both declared bankruptcy in 2016, and among the specialty retailers you saw Sports Authority close its doors last year. We are also seeing store closures from other retailers. For example, Macy’s, Office Depot, and Sears each have plans to close at least 100 stores, on top of closures in prior years. Stores are not completely going away anytime soon, especially for products where consumers want a hands-on experience. But in an omnichannel world, stores are not the only shopping destination.

With the rapidly growing utilization of mobile devices, we anticipate the concept of “showrooming” will only continue to grow. This refers to consumers who go to a store to touch and experience a product, while conducting product research and price comparisons online. Even Amazon has played into this trend, with the launch of several physical locations, including book stores, pop-up retail locations, and, most recently, a grocery store.

What is the consumer buying?

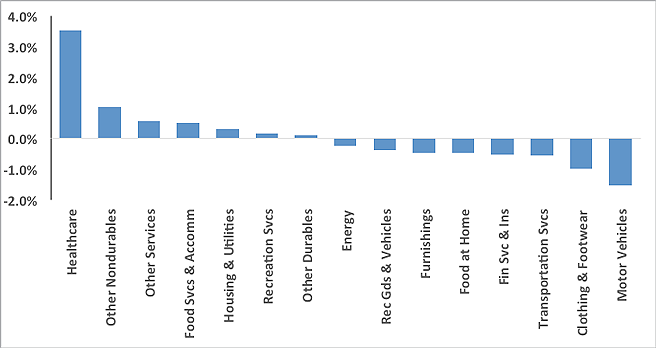

The consumer is focused on value. This is in part driven by changes in the retail landscape, as the omnichannel and digital experience provide price transparency. We’re also continuing to see other shifts in consumer spending patterns. For instance, consumers are spending more on “experiences” rather than “things,” and that has altered the total mix across discretionary categories. As illustrated in the chart below, we are seeing smaller allocations to traditional goods like clothing and groceries, while spending on food services, accommodations, and travel and entertainment are growing. One of the newer trends over the past few years has been the growth of the sharing economy (Airbnb, Uber, Lyft, etc.), which has created an open marketplace for consumers and, in the process, disrupted the traditional vendors in these sectors. This has added yet another catalyst to support consumers’ ongoing hunt for value.

Additionally, millennials are beginning to have families. Household formation is increasing and we are seeing steady growth in spending on housing and home improvements. Additionally, rising health care costs have required consumers to adjust their spending behaviors.

Shift in Consumer Wallet By Major Category

Change in nominal consumer wallet allocation, 2000-2015

What retail formats are best positioned for growth?

Given the shifting consumer behaviors, the outlook for e-commerce remains very favorable. Several trends are providing a tailwind for those retailers that can provide a seamless experience for consumers. In particular, growing mobile utilization and the focus on value should benefit industry-leading online retailers, while the struggles of brick-and-mortar names will only accelerate for those that can’t match the value and convenience of newer entrants. While not currently the best positioned for growth, traditional retailers are playing catch up by investing heavily to expand their online presence. They are also offering differentiated services, such as buy online/pick-up in store and buy online/ship from store in an effort to be omnipresent to the consumer.

Other formats that are well positioned include discount-oriented stores that provide value, and home-improvement stores that are benefiting from demographic trends and macroeconomic factors. Even as interest rates were hiked in December, the outlook for housing remains favorable. This is in part due to rising household formation and millennials moving into their 30s, which has traditionally been the prime home-buying age.

How is ADX positioned to benefit from these trends?

Our holdings include internet retailers Amazon and Priceline, discount-oriented retailers Dollar General and Wal-mart, home improvement retailer Lowe’s, and Starbucks. Amazon is well-positioned to continue to reap benefits from its product breadth, assortment, and logistics expertise, as well as from its loyal Prime membership base. Recent portfolio addition Priceline, an online travel agent with a vast global footprint of properties and services, offers an attractive growth profile and should continue to benefit from the growing consumer spending preference for “experiences.” Another “experiential” holding is Starbucks, which gives us exposure to an iconic brand with significant expansion opportunities across geographies, product offerings, and an industry-leading customer-loyalty program.

What is the outlook for the consumer?

While there are a number of factors affecting the consumer, the outlook is favorable. The Trump presidency is likely to result in tax relief at the personal and corporate levels, which may bolster consumer spending. Easier access to credit may further stimulate spending. However, the potential for protectionist measures such as increased taxation of imported goods and other input costs may cause price inflation for certain items such as apparel. Rising gas prices and mortgage rates may also offset some of the stimulus mentioned above. Considering all of these factors, we expect consumer spending to grind higher in 2017.