It’s not that stock selection doesn’t matter, but asset allocation has a far bigger impact on long-term performance.

By Mark Stoeckle

August 20, 2018

When people talk with their friends and colleagues about investing, they invariably focus on individual stock trades that have made them money. After all, it's no fun to talk about losing money on stocks. While discussing individual stock trades makes for good small talk, it is the less glamourous aspect of investing, known as asset allocation, that can be a key determinant of long-term performance.

Asset allocation refers to how investors allocate their money among various investment vehicles such as stocks, bonds, real estate, gold, cash, and other investments. By investing in several different types of assets, the risk associated with a single one is reduced. A well-diversified asset allocation strategy strives to reduce the overall volatility of the portfolio by spreading risk over a number of investments.

Given that asset allocation is a fundamental component to long-term investing, rebalancing assets is critical to ensure the level of risk remains consistent with an individual’s investment strategy.

To create a diversified portfolio, investors combine assets whose returns have not historically moved in the same direction. This way, if a portion of a portfolio is declining, the rest of the assets may be growing. The goal is to offset some of the impact that an underperforming asset can have on an overall portfolio.

To create an optimal asset allocation for individual investors, advisors consider personal goals, risk tolerance, and investment time horizon to construct a portfolio. Younger investors generally have a longer time horizon and can take on more risk as they are focused on building wealth. These investors may be looking for growth-oriented investments and as a result, will generally incorporate more equities into their portfolios. On the other hand, older investors may need access to their money sooner and may prefer less risky investments. Portfolios for these investors often overweight fixed-income securities to protect assets during periods of uncertainty.

Asset allocation can be as simple as a portfolio made up of 70% stocks and 30% bonds, or something far more complex, incorporating several different asset classes with diversified exposure across geographies, market capitalizations, and asset types.

The various strategies around asset allocation rarely make for must-see television. But these considerations have an outsized impact on performance and in many cases, the impact is far more pronounced than most investors realize. According to one study1 analyzing the returns of corporate pension funds, researchers found that approximately 90% of performance variability was attributable to asset allocation decisions. Subsequent studies2,3, meanwhile, have pegged the return variance as ranging from as low as 33% to as high as 75%. While academics may debate the exact impact, what no professional investor would dispute is that asset allocation is an important determinant of investment performance.

Given that asset allocation is a fundamental component to long-term investing, rebalancing assets is critical to ensure the level of risk remains consistent with an individual’s investment strategy. This is particularly the case during years in which one asset class outperforms another by a wide margin, such as 2017, when equities vastly outperformed fixed-income securities. Since equities at the close of the year would represent a larger portion of the portfolio than the original allocation strategy in January, rebalancing at regularly intervals, such as annually, ensures that investor portfolios remain aligned to their goals.

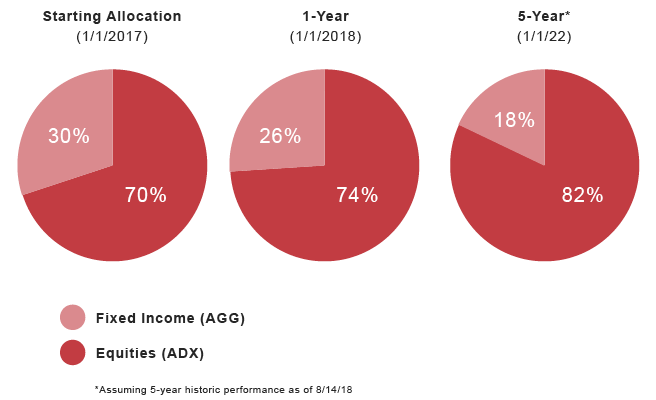

The following charts highlight allocations to Adams Diversified Equity Fund (ADX) and iShares Core U.S. Aggregate Bond ETF (AGG). In just one year’s time, a 70/30 equity-to-bond allocation nearly became a 75/25 allocation given the nearly 30% returns in the ADX fund in 2017. Over a five-year period, assuming historic averages, the allocations of a 70/30 original investment strategy would become approximately 80/20 without rebalancing.

Allocation Changes Without Rebalancing

Rebalancing is also important as investors move through the various stages of life and their needs change. The level of risk that is appropriate for younger investors fresh out of school tends to be far more than what is appropriate for retirees living on a fixed income.

In past Insights in our “Stay Invested” series, we’ve highlighted the challenges of trying to time the market and why a long-term mindset can be so valuable to investors. This is particularly the case during periods of volatility and in an era in which a glut of information makes it nearly impossible for individual investors to decipher the real market signals from the noise.

So while the day-to-day gyrations of the market, or a 24/7 news cycle, may tempt market watchers to continually recalibrate, investors would be wise to stay invested and rebalance their portfolios at regular intervals to ensure their investment strategy remains aligned to long-term goals.

2 Sector, Style, Region: Explaining Stock Allocation Performance, Raman Vardharaj, Frank J. Fabozzi, https://www.cfapubs.org/doi/pdf/10.2469/faj.v63.n3.4691

3 The Importance of Asset Allocation, Roger G. Ibbotson, https://www.cfapubs.org/doi/pdf/10.2469/faj.v66.n2.4